Links 2024-04-17 - Shouting From The Rooftops, or . . .

Tilting at Windmills

The common thread today is that I know I’ve linked to and posted about this important work before, but I will continue shouting it from the rooftops until it sinks in.

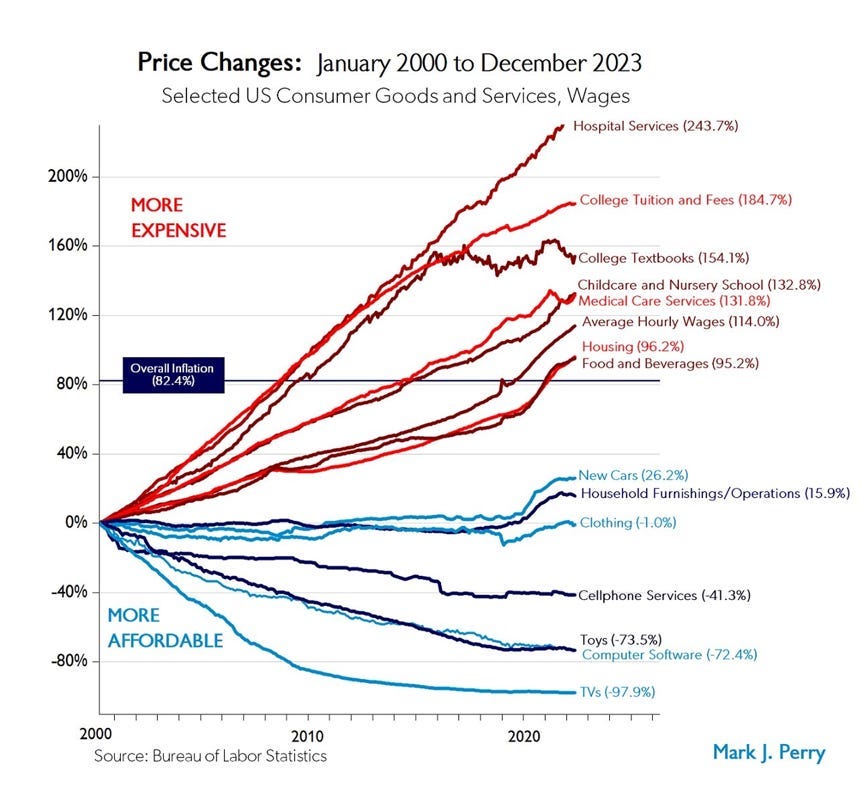

The first is from Gale Pooley writing at Human Progress. Building off of Mark Perry’s famous chart of historical price changes from various categories of consumer goods (captured below), Pooley combines it with his work on time prices to demonstrate what the actual abundance change has been.

As Pooley writes,

Over this 23-year period, overall inflation increased by 82.4 percent while average hourly income increased by 114 percent. Hourly income increased 38 percent faster than prices. This indicates a 14.8 percent decrease in overall time prices. You get 17.3 percent more today for the same amount of time 23 years ago.

This illustrates the fact that things can get more expensive and more affordable at the same time. As long as hourly wages are increasing faster than product prices, time prices are decreasing, which is another way of saying personal abundance is increasing.

The second is from Art Carden writing at Econlib where he gives a succinct book review of The Myth of American Inequality: How Government Biases Policy Debate by Phil Gramm, Robert Ekelund, and John Early. The common narrative (conventional wisdom) on income inequality is the U.S. is flat out wrong. From Carden,

“Their empirical message is also simple but a lot more controversial:

There are certainly people who are physically or mentally unable to care for themselves and have fallen through the cracks in the system that delivers transfer payments, but, for all practical purposes, poverty due to a lack of public or private support has been virtually eliminated in America. (p. 4)

The post-tax, post-transfer poverty rate, they argue, is not the 12.3% the Census Bureau reported in 2017, but about 3%.”

The third and fourth are from Kevin Erdmann writing at his Substack. He begins by offering A Brief Technical Review of the Alternative Housing Story.

More than in the other cases, I guess I will have to keep linking to this work until you people get it through your heads that the popular narrative of the Great Recession (including that of the experts) is dead wrong.

We built !TOO FEW! houses in the critical places, had a moral panic regarding rising housing prices (a symptom) and mortgage access, declared credit de facto illegal for all but the highest-rated borrowers, misinterpreted inflation data in a way that conveniently corresponded to the moral panic causing the Fed to tighten monetary policy to unprecedented Great Depression levels, and only then from all that caused a fantastic chain reaction that resulted in a lot of bank investments that were under appreciated for their riskiness to go sour. In basically that order.

N.B. A lot of the medicine to help alleviate the problems was counter productive (crowding out) at the time and set the stage for future problems (moral hazard).

Next he demonstrates how 2024 is the counterfactual to 2009.

From his conclusion,

To reiterate the earlier point, 2024 is actually what 2007-2009 could have and should have looked like. If you want to know how America could have avoided a $5 trillion highly regressive wealth shock without the moral hazard of constantly bailing out dumb money, the answers are all tragic and ironic.

It was 2008 that required bailouts. Nobody’s asking to bailout Austin real estate investors in 2024. The moral panic created the demand and need for bailouts. If the mortgage crackdown hadn’t happened, and if the Fed had aimed for a recovery in construction and home values, there would have been a real estate bust in the Contagion cities, for better or worse. Some real estate speculators there would have taken a bath, and there would never have been trillion dollar rescue packages.

If you’re pro-mortgage crackdown, then, in practice, you’re pro-bailout. Don’t pat yourself on the back for complaining helplessly about the bailouts your favored policies necessitated.

Of course, the people that were hurt the worst, not of their own actions, didn’t get bailouts. Hurting them was the point, or was the unintended result of whatever the point was supposed to be, because the collapse in the prices of their homes was the goal. You could take the Rick Santelli tea party stand and say “screw them” or you could take the Occupy Wall Street stand and say, “It’s the bankers’ fault” and take the self-satisfied incoherent position that we should somehow simultaneously enforce 50% declines in valuation by locking families out of mortgage access while also subsidizing those families for the $5 trillion loss.

Now that all of that is settled, on to new dragons to slay . . .